Getting rich, having access to powerful people, controlling people’s financial destiny and having tangible expensive signs of status easily available to you is intoxicating. It can, like any drug, become hard to live without and encourages a muddle-headed notion that you are entitled to it, you deserve it.

The trail of destruction of this type of myopically selfish behaviour of the many in the Australian financial sector was revealed over the year-long Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry.

Ken Henry, Chair of the National Australia Bank, spelled it out in his testimony to the Royal Commission, that somewhere in the neoliberal takeover of the world’s markets of the last 40 years, the PURPOSE, or ends, for a business to exist was to make as much money as possible for those with access to other peoples’ capital. This became more important than providing a suitable, useful or valuable good or service that people wanted to buy.

And unsurprisingly, the Australian financial sector lost its way as it prioritised getting another hit of ‘more’. More money for themselves. More power. More privilege. More stuff.

When a business’s primary purpose or ‘end’ is to provide a good or service that is valuable to and valued by its customer, there is a clear destination. A business can measure how many times it achieves it, how it can improve on it or adapt itself to meet customer requirements. There is a clear compass.

When a business’s ‘end’ turns inward exclusively prioritise its own enrichment, then it has no external reference point, no definitive destination to be reached. More and more is better, greed is good. The end justifies any means to get there, because there is no such thing as enough.

The financial institutions preyed on people’s lack of understanding of their essentially intangible product and, in a display of breathtaking hubris and arrogance, converted the concept of caveat emptor (buyer beware) into ‘we are going to fleece the dumb suckers’ because they felt entitled to do it and it gave them another hit.

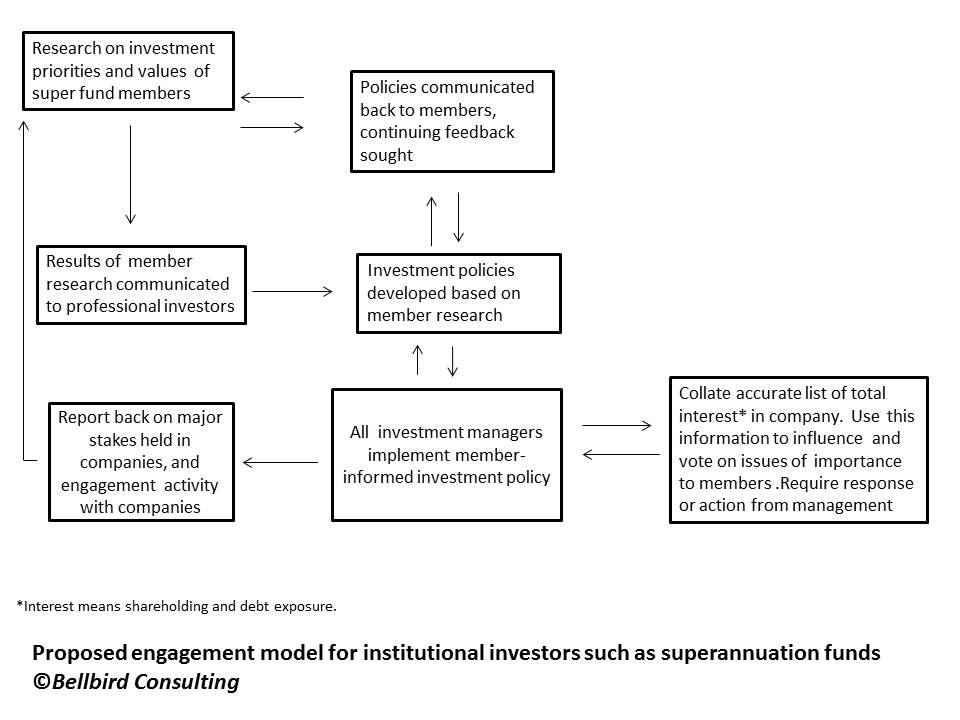

The financial institutions also gave a privileged seat to the professional investment teams that provide them the capital they need to exist. These investors, at an arm’s length away from the customers and the employees, focused solely on their investment returns, driving short-term profits to meet their own targets for personal enrichment.

In order to avoid repeating this process over and over, the people with the power to change the destination must want it to change. They must accept that their short-term binge for self-enrichment will ultimately weaken the financial system. They need to accept that they are not inherently entitled to create wealth for themselves at the expense of customers and employees.

A sustained shift to a customer-focused, ethical approach to providing access to capital for businesses and people to thrive is required. Banks and other service providers must understand that there are limits on what they deserve in payment for providing that service.

And we all must accept that the drug of ‘more and more’ is not good for any of us.