Most financial service professionals believe tighter regulation of financial markets will not stop another financial crisis, according to a recent survey.

Perhaps a reminder of what happens when greed overtakes reason might help. Today the ratings agency Standard and Poor’s said it estimates that the biggest US banks may still have to pay out more than $US100 billion to settle legal issues surrounding the rush for sub-prime mortgage products that started the global financial crisis in the first place. Not a great long-term return for the banks’ investors.

Or maybe a reality check about what their rampaging greed has meant for the rest of the citizens of the world. The Organisation for Economic Co-operation and Development (OECD) is warning that the fallout of the financial crisis, is starting to affect the elderly with lower and delayed pension payments and the gap between the highest and lowest income households in developed countries widened in the three years since the crisis.

Sadly, the only way to affect real change in behaviour is to change the values of those in power, because it is those in power that set the agenda. Kinetic Partners, the same group that conducted the survey mentioned above also did research that found that most believed it was the culture set by the CEO that influenced whether good decisions were made and another financial crisis could be averted. This is backed by a whole swathe of academic research pointing to the powerful elite prioritising the values of our society.

So what are the most prominent values? Academics Bruno Dyck and David Schroeder suggest materialism and individualism are the twin hallmarks of the moral point of view that underpins management thought. The Protestant focus on work and individual struggle for salvation and emphasis on material success has become normalised in western management and is the ‘incontestable, objective, morally neutral reality’ adopted as the natural facts of life, rather than the moral facts of life. This translates into modern management’s focus on efficiency, productivity, profitability relative to other comparable companies and the expectations of the market.

The central criterion for managerial rhetoric is concerned with economic growth, organisational survival, profit and productivity. In academic texts on corporate finance this belief is reinforced. According to the Principles of Corporate Finance, ‘the goal of maximising shareholder value is widely accepted in both theory and practice’ because, the authors argue that shareholders want three things, the first of which is ‘to be as rich as possible’. Another perspective on this is offered by Jill McMillan who argues that companies are held captive by ‘the tyranny of the bottom line’ and profits are for the benefit of the ‘privileged class of organisational shareholders who possess the dominant right to maximise return on their investment and the commitment of management to pursue that goal.’

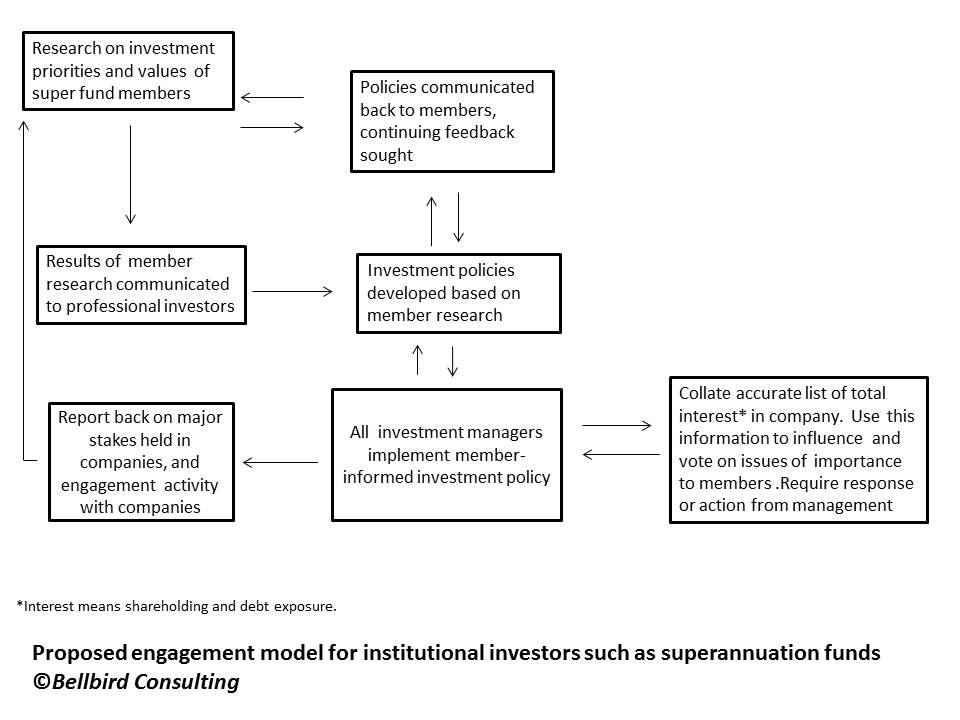

But if much of the money is invested with ‘organisational shareholders’ (meaning institutional investors) comes from citizens investing for their retirement, then it should be us that guides which values dominate investment, and given a chance to have a say, I believe many people would have not ‘profit at all cost’ as their number one value.

Below is a simplified version of my suggested model for a two-way communication system with their members.

Related articles

- Corporate Psychopaths, did they cause the financial crisis? – a critical looks at Boddy’s 2011 Corporate Psychopath Theory (rhortonblog.wordpress.com)

- Swensen criticizes Wall Street (yaledailynews.com)

- Financial Scandals, Regulation and Democracy (ihrrblog.org)