Laura D’Olimpio argued in her recent article on The Conversation, that the ancient Greek philosopher Aristotle claimed that being virtuous was rational and good for everyone. Humans, he wrote, are political and moral creatures because we live in a society and our behaviour affects one another. Virtue is the mid-point between excessive or deficient behaviours and finding the mid-point was crucial for everyone to flourish. For instance, we may have to pay $5 more for a T-shirt, and a large Western organisation may need to take a small cut to its profit margin in order for garment workers in Bangladesh to have a safe working environment and enough money to support the family. But everyone still wins because we still get cheap t-shirts, the business still makes money and people in Bangladesh improve their quality of life through economic growth.

But the spectre of renowned free marketeer economist Milton Friedman still looms over the financial markets and listed companies. Friedman believed in the view that the only social responsibility of business was to make profits’ is still a dominant belief among large investment houses and the companies they invest in. Therefore, maximising profits is a seen as a virtue in this world.

Indeed, Max Weber, as cited in Dyck and Schroeder’s 2005* article, wrote that materialism and individualism are the twin hallmarks of the moral point of view that underpins management thought. A focus on work and emphasis on material success has become normalised in western management and is the ‘uncontestable, objective, morally neutral ‘reality’’ adopted as the natural facts of life, rather than a particular version of the ‘moral’ facts of life. This translates into modern management’s focus on efficiency, productivity, profitability, measured by performance relative to other comparable companies and the expectations of the market.

Materialism is used as a tool to measure human progress, a method of attaining ‘success’ and social acceptance. In 2010, Decktop, Jurkiewicz and Giacalone** argued that financial success and material possessions are the core elements of western corporate cultures and financial rewards at work are used as a form of motivation and control. Materialistic values are rewarded in employees because they are aligned to those in senior management. In this view, money and the desire for money equal competence and the acquisition of more of it (particularly more than someone else) equals greater competence. People with these values gravitate to jobs that can be measured by material accumulation. In corporate finance books this belief is reinforced. According to the Principles of Corporate Finance, ‘the goal of maximising shareholder value is widely accepted in both theory and practice’ because, the authors argued that shareholders’ priority is ‘to be as rich as possible’ (Brealey, Myers and Allen 2011). The question of ‘why is this important?’ is not considered.

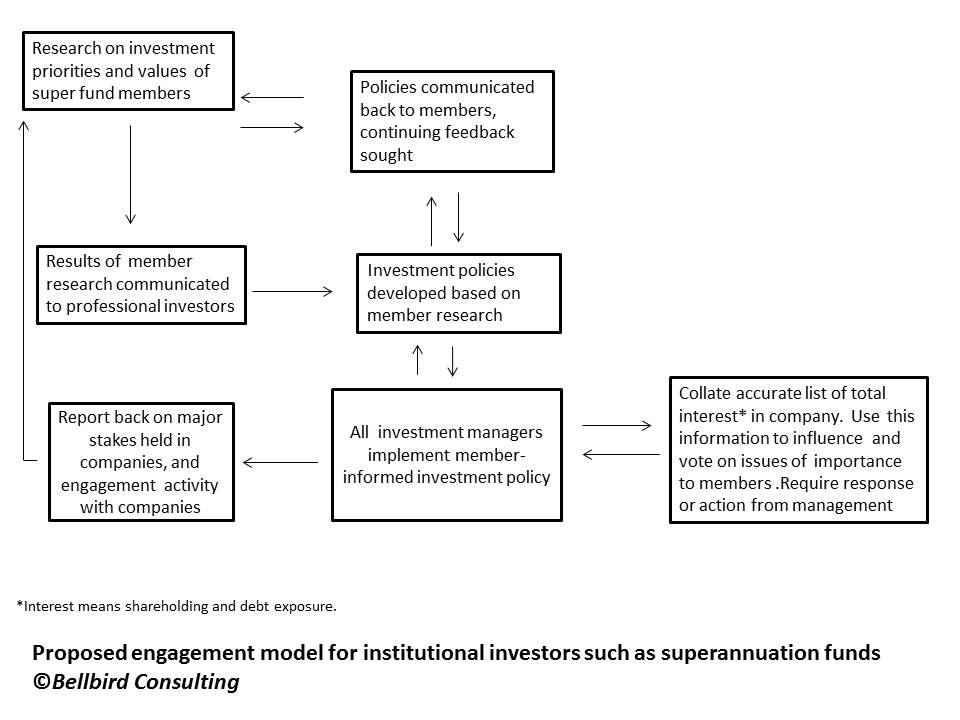

Companies are held captive by the tyranny of a quarterly earnings reporting cycle that focuses on short-term profit making rather than long-term sustainable business development. This benefits the privileged class of institutional investors who make their money by managing trillions of dollars of other citizens’ money. They market their competence as investors to attract more money, based on these short-term returns. When the reality is most of their investors have a very long-term investment timeframe and quarterly results are not particularly relevant.

This mismatch in expectations between the average citizen whose retirement funds are managed by institutional investors, and the investors and senior managements of companies themselves is demonstrated in the recent research by Harvard Business School and Chulalongkorn University. The research showed that the average citizen around the world believes that CEOs earn far more than what is a fair amount, when compared to an unskilled workers. What was worse is that the estimate was completely out of kilter with the astronomical pay packets that actually get paid, which is supported by most fund managers.

Surely this is an example of one group, the powerful elite who manage and influence the management of large listed companies, who’s values are at the extreme end of a spectrum, and the virtuous mid-point which allows everyone to flourish is a long way, away.

*Dyck, B. and D. Schroeder. 2005. “Management, theology and moral points of view: Towards an alternative to the conventional materialist-individualist ideal type management.” Journal of Management Studies 42(4): 705-735.

** Decktop, J., C. Jurkiewicz, and R Giacalone. 2010. “Effects of materialism on work-related personal wellbeing.” Human Relations 63(7): 1007-1030.