I recently finished reading What Happened to Goldman Sachs: An Insider’s story of organisational drift and its unintended consequences, Steven Mandis’s study of how the priorities of one of Wall Street’s most respected investment banks changed from providing trusted advice about long-term growth of businesses to short-term profit production for its employees and shareholders.

As a former Sachs employee, Mandis was curious about how the Goldman Sachs he joined in the 1990s, which was renowned for its customer-centric ethics and social code, turned into the one of the morally questionable actors of the global financial crisis. It tracks the drift in values since the 1970s and covers a period of rapid growth for the company and the financial services industry.

Mandis noted (pg 98) that the rapid growth in Goldman’s business meant thousands small decisions, made quickly and by many, accumulated into a significant tidal wave of change, and everyone was too busy to notice. Changes included the rise of a culture of undisciplined risk taking driven by the rising prominence of profit-making trading over advice and the dilution in the strength of its cultural norms as the business expanded quickly around the world.

More importantly it highlights the shift from banking to trading (pg 143) and how, as trading produced greater profits for the bank (rather than the clients), the culture shifted from ‘value-added vision and tilt more to making money first’ and asked the question ‘if making money is your vision, to what lengths will you not go?’.

Mandis examined what pressures existed to meet organizational goals generally caused by ‘unintended and unnoticed slow process of change in practices and the implementation of them, which in those cases led to major failures.’ This can be expanded out to the whole investment industry which, when inundated with the retirement savings of ordinary citizens into their mutual funds, suddenly had more sway with the companies than ever before.

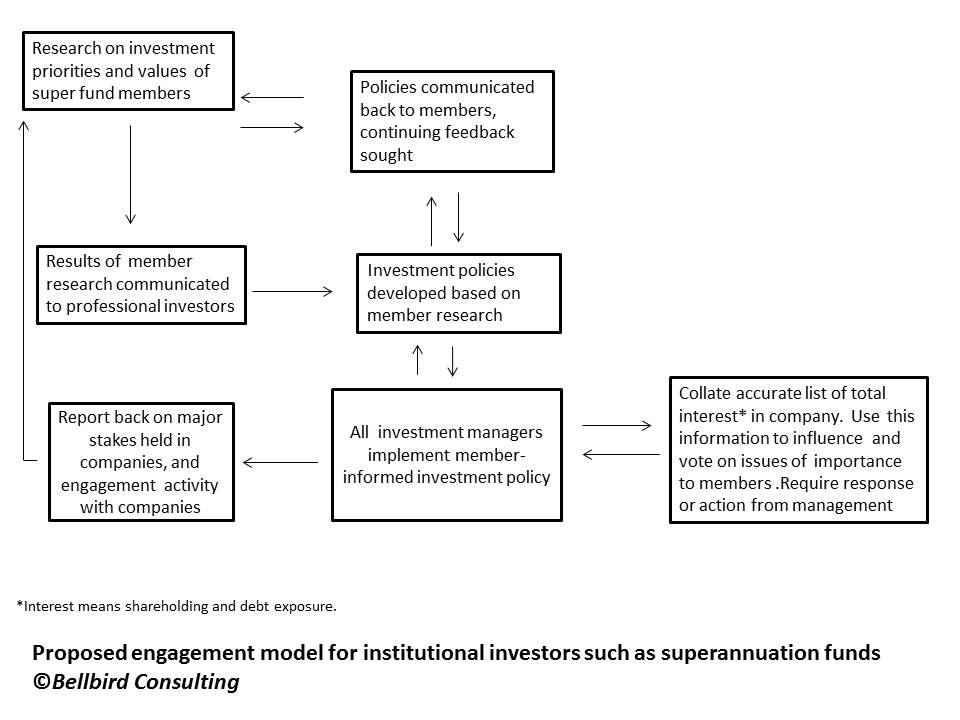

Fund managers, wielding the investment power of the accumulation of many citizens’ funds, held more sway with company management. The power for decision-making, and the shaping of global business, resides with a small group of senior managers who make decisions with reference only to a small group of professional investors, i.e. decisions are made by those who manage the money, rather than those who provide and ultimately own the money. It is the beliefs and values of the professional investors that are represented, not those whose capital offers the companies the opportunity to continue business and the superannuation funds a chance to have a business.

Indeed, it is telling when the chief executive of the world’s largest miner BHP Billiton describes spinning off a basket of its lesser performing assets into another company as a way of ‘financial markets’ being happy. No mention is made of the values and views of the citizens’ that provide the capital to the financial markets.

It is also interesting to note that an independent senator in Australia’s parliament, Nick Xenophon, chooses to focus on the decision of the nation’s flag carrier Qantas to only consult with its largest institutional investors about controversial management decisions, rather than include the large number of smaller shareholders. He would perhaps, have been well served to question why the big institutional shareholders made no effort to listen to the views of the thousands of citizens who provide the capital to invest in Qantas. These are the citizens who may also work for Qantas, or are a supplier or contractor to the airline, or even are a frequent flyer.

It is time that large asset management houses created genuine engagement programs with their members to discovery what their investment values really are, in the context of the whole society, not just how much money they want to retire on, and base some of their decisions on that ethical compass, rather than the one that points only to the god of Mammon.