Western Australian Premier Colin Barnett sent a shot across the bow of the oil and gas companies that operate off the Western Australian coast at a recent industry conference in Perth by challenging their notion of social licence.

Financial journalists and politicians looking for a hook to hang him on immediately started to quibble about some of the factual detail around ownership of leases and completely missed the opportunity to debate the broader point, on which Mr Barnett was right. That is, companies do need to seriously look beyond their own bottom line at how they treat the Governments and communities in which they operate and provide more of a legacy than local libraries and playgrounds.

The fraught issue of who profits from oil and gas extraction and how they profit must be seen from a multilayered perspective and how we see it is clouded by an increasingly outdated notion of stakeholder theory.

Stakeholder theory is the basis of how many businesses engage with various ‘stakeholders’ and their interests. For example, groups get divided into ‘shareholders’, ‘customers’, ‘government’, ‘activist groups’ and ‘local community’. Then they are usually separated and ranked according the importance to the senior management. For large listed entities, the very top of the tree is usually shareholders (to which I mean large institutional investment groups who manage money on behalf of others), and meeting the demands of this prioritized group(s) can be the greatest influence on decision-making.

What stakeholder theory overlooks is that most stakeholders belong to more than one group, who may ‘profit’ or lose in more than one way, and who the stakeholder really is may be obscured at first glance. For example, oil and gas resources in Australia, including coal seam gas, are owned by the relevant State or Territory government or Federal Government (depending on whether it is onshore or offshore) on behalf of their citizens. The relevant government then grants licences to companies to explore and extract these resources and ‘profit’ on behalf of their citizens through the collection of royalties.

So the owners of the assets are the citizens of the relevant State, Territory of Australia or Australia itself and they profit through: the collection of royalties; the access to the resource they own (domestic gas supply); and community economic development through job creation. This same group may also ‘lose’ if the extraction of resources unnecessarily damages their environment or the opportunity cost of losing other industries, such as agriculture, fishing or tourism is seen as too great.

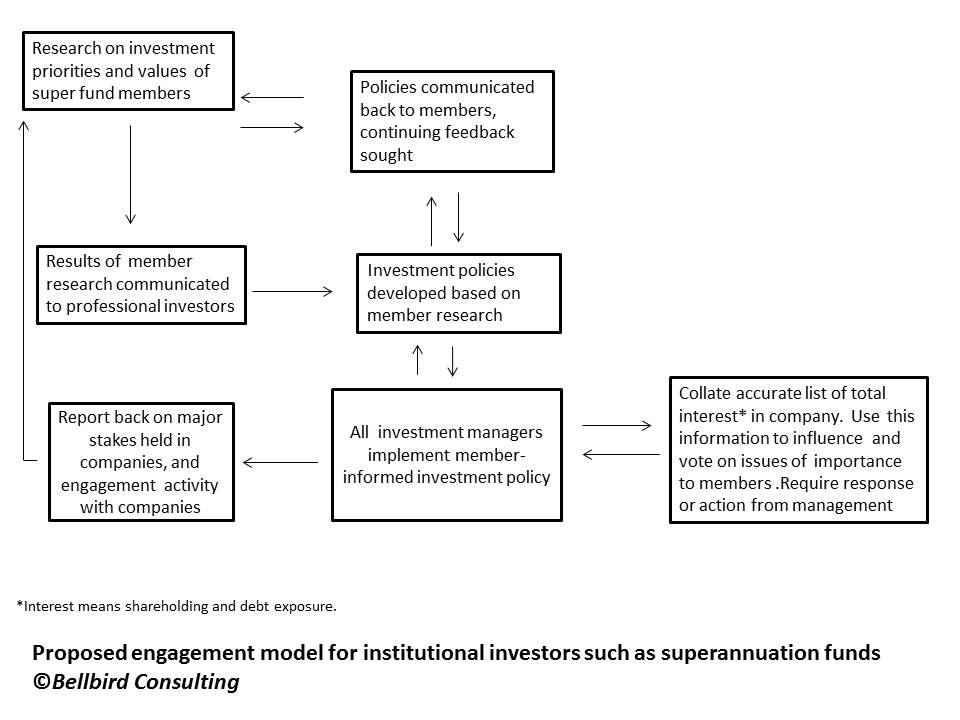

While the oil and gas extraction companies will say their fiduciary duty to place shareholders first, they may not recognise that the capital provided to institutional shareholders to whom the oil and gas companies are trying to deliver a profit are some of the very same citizens who own the resources they extract. The capital flow comes through savings such as superannuation funds and other retirement savings.

For example, the coal seam gas enterprise Arrow Energy is a joint venture owned by Royal Dutch Shell plc and PetroChina Company Ltd. As a 14 February this year, Shell stated in its 2013 Annual Report that major investment houses such as Blackrock and The Capital Group owned more than 6% and 3% respectively. In turn, Blackrock on its website states in runs $US4.3 trillion in investments around the globe on behalf of ‘governments, companies, foundations, and millions of individuals saving for retirement, their children’s’ educations and a better life’, including Australian citizens. In this scenario the citizens ‘profit’ through the increase in share price and payment of dividends.

The offshore oil and gas activities in the north west of Western Australia are dominated by majors such as Shell, Chevron and Woodside all of whom are large listed companies with institutional shareholders, who would manage the millions of dollars of individual savers. These are the companies at which Mr Barnett was taking aim, particularly after the decision to develop an offshore floating processing plant, rather than base it onshore in Western Australia and create opportunity for the local communities.

Oil and gas companies need to consider how to balance all of these streams of ‘profit’ more evenly and consider opinions beyond the institutional shareholders who manage citizens’ money, often without reference to their views. They may also need to learn to find value in the competing view that their citizen stakeholders’ don’t necessarily wish to ‘profit’ from the extraction of resources but would rather use the land and sea for other means, such as agriculture, or even to leave the environment untouched.